# Summerstone (https://summerstone.xyz/index.md)

Expanding onchain markets.

Summerstone builds infrastructure for onchain markets with production systems across borrowing, yield, liquidity, and research.

## Primary pages

- [Borrowing](https://summerstone.xyz/borrowing.md): Automated borrowing for Liquity-based protocols.

- [Yield](https://summerstone.xyz/yield.md): Curated yield strategies and vault frameworks.

- [Liquidity](https://summerstone.xyz/liquidity.md): Market operations and execution tooling.

- [Research](https://summerstone.xyz/research.md): Long-form publications and market analysis.

- [Blog](https://summerstone.xyz/blog.md): Announcements and ecosystem updates.

- [Documentation](https://summerstone.xyz/docs.md): Product documentation and guides.

# About Summerstone (https://summerstone.xyz/about.md)

We excel at the intersection of onchain markets, realtime data and quantitative and agentic algorithms.

## Vision and mission

Summerstone is focused on expanding fair, efficient, and predictable onchain markets for people and businesses worldwide.

## Values

- Reliability: production-first engineering and operational rigor.

- Security: defense-in-depth and explicit risk management.

- Focus: solve a few hard problems exceptionally well.

Related pages: [Borrowing](https://summerstone.xyz/borrowing.md), [Research](https://summerstone.xyz/research.md), [Docs](https://summerstone.xyz/docs.md)

# Effortlessly optimized borrowing (https://summerstone.xyz/borrowing.md)

Summerstone is the leading provider of set-and-forget interest rates on Liquity-based borrowing markets.

## Product overview

Automated Borrowing automates interest-rate adjustments for collateral-backed loans while preserving user custody.

## Supported protocols

- Liquity V2 (BOLD, Ethereum): [docs](https://summerstone.xyz/docs/borrowing/supported-protocols/bold-and-liquity-v2.md)

- Nerite (USND, Arbitrum One): [docs](https://summerstone.xyz/docs/borrowing/supported-protocols/usnd-and-nerite.md)

- Soneta (ONE, Sonic Mainnet): [docs](https://summerstone.xyz/docs/borrowing/supported-protocols/one-and-soneta.md)

- Mustang (MUST, Saga EVM): [docs](https://summerstone.xyz/docs/borrowing/supported-protocols/must-and-mustang.md)

## Guarantees

- Self-custody delegation.

- Protocol-enforced fee/adjustment constraints.

- Gas costs for adjustment execution covered by Summerstone.

# Summerstone Documentation (https://summerstone.xyz/docs.md)

# Overview (https://summerstone.xyz/docs/borrowing.md)

Summerstone’s rate automation solution is designed specifically for users who value:

* **Self-custody:** Retain full control of your funds at all times.

* **Efficiency:** Automated adjustments eliminate manual work, reducing stress and costs.

* **Transparency:** All actions and parameters are fully verifiable directly onchain.

Chat with our docs using an LLM using [this LLM-friendly text file](https://summerstone.xyz/llms-full.txt) of the full documentation.

## Security and Transparency

All parameters are verifiable onchain, providing absolute transparency and security:

* **Fixed Service Fee:** A maximum fee of 0.3% annually.

* **Adjustment Frequency:** Normal adjustments no more frequently than once per week.

* **Immutable Guarantees:** Parameters enforced by smart contracts.

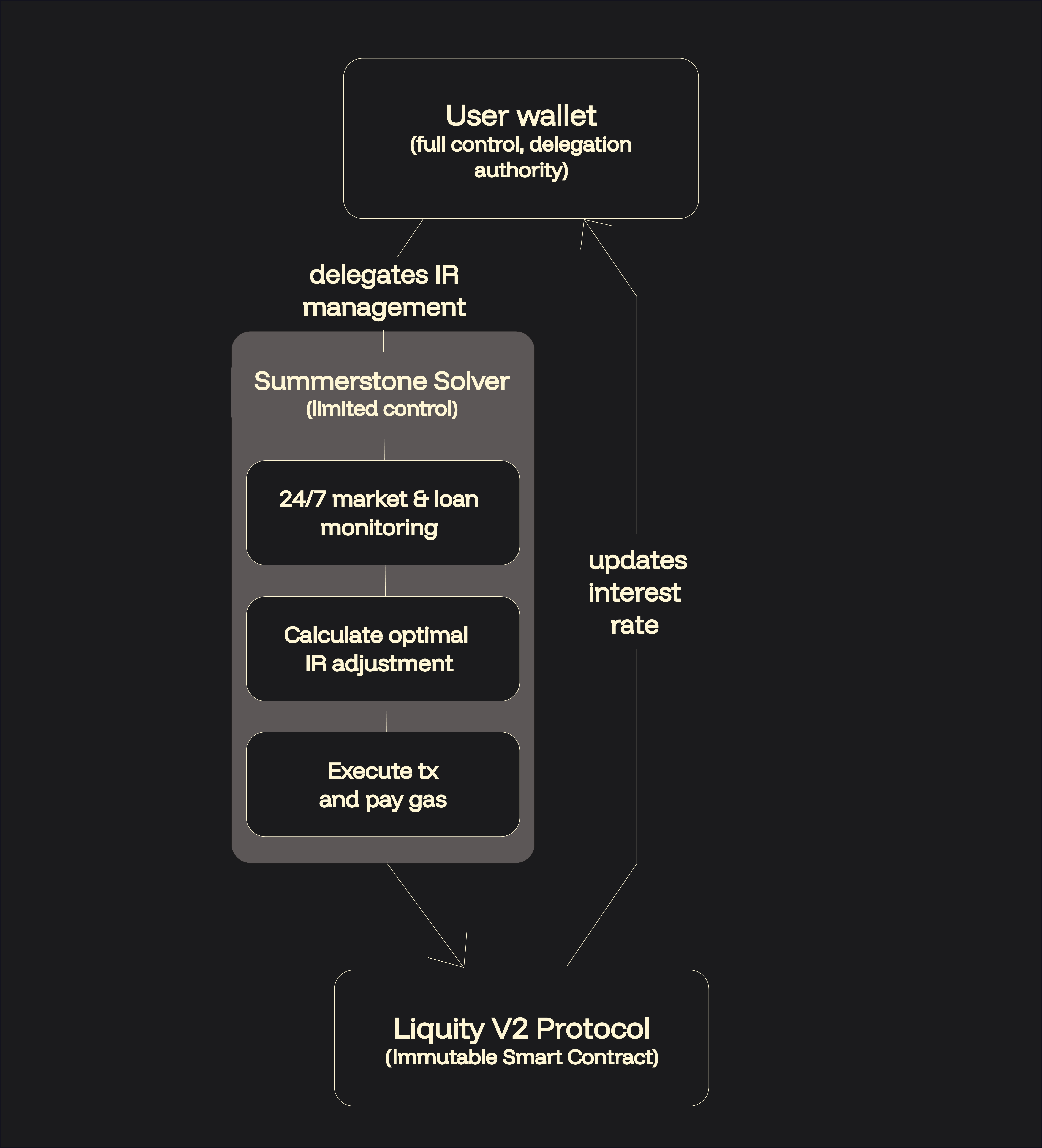

## How the Automated Adjustment Process Works

The following diagram illustrates how Summerstone’s automated interest rate strategies interact with loans and the Liquity-V2-based protocols:

### Explanation of the Diagram:

* **Delegation:** You delegate authority to adjust your loan’s interest rate (no fund custody involved).

* **Monitoring:** Our algorithm constantly evaluates market conditions, including debt positions, redemption risks, and gas conditions.

* **Adjustment Calculation:** The solver computes the optimal interest rate adjustments based on your preset risk strategy.

* **Execution:** Adjustments are securely executed directly on the Liquity V2 protocol, reflected transparently onchain.

## Getting Started:

1. Open your loan settings in a supported frontend of your chosen protocol.

2. Delegate interest rate automation to our verified address. Check our [supported protocols](/docs/borrowing/supported-protocols).

3. Confirm the transaction - your loans are now fully automated.

# Frequently Asked Questions (FAQs) (https://summerstone.xyz/docs/borrowing/frequently-asked-questions.md)

## What exactly does Summerstone do?

Summerstone provides automated interest rate adjustments for your Liquity V2-based loans. By continuously monitoring market conditions, our system optimally adjusts your interest rate to keep borrowing costs low, proactively minimize redemption risk, and eliminate the hassle of manual adjustments.

***

## How do automated interest rate adjustments work?

Our system monitors key metrics continuously, including:

* Redemption risk and debt positions

* Market price fluctuations

* Network gas conditions

* Liquity protocol status and events

Based on these metrics, our algorithms determine precisely when and how to adjust your loan's interest rate, optimizing your borrowing efficiency.

***

## How much does Summerstone cost?

We charge a straightforward 0.3% annual service fee based on your total loan amount, enforced transparently by the protocol. For most users, these costs are offset by:

* Reduced gas expenses from eliminating manual adjustments

* Lower average interest rates

* Reduced risk of redemption penalties

You can calculate your exact potential savings using our [Savings Calculator](/docs/borrowing/savings-calculator).

***

## Is delegating interest rate adjustments secure?

Yes. Delegation through Liquity V2 protocols is inherently safe and limited:

* Delegates / batch managers **only** have the ability to adjust interest rates.

* Delegates / batch managers **cannot** access or transfer your funds or modify other loan parameters.

* Delegation permissions and boundaries are verifiable directly onchain.

***

## Can Summerstone guarantee protection against redemptions?

While our automated system significantly reduces the likelihood of redemption by proactively adjusting rates, we cannot guarantee complete protection due to inherent market volatility and liquidity factors.

Please review our comprehensive [Terms of Service](/docs/borrowing/terms-of-service) to understand these risks fully.

***

## Which frontends can I use?

Liquity does not run its own frontend. You can use any frontend that supports interest rate delegation for Liquity V2 protocols. You can find independent frontends [here](https://www.liquity.org/frontend-v2) or just head to [liquity.app](https://liquity.app/).

***

## How frequently are interest rates adjusted?

Adjustments typically happen at most once per week under normal conditions. During high-risk periods, adjustments may occur more frequently as needed, within the limits enforced by the Liquity protocol.

***

## Do rates differ based on collateral types?

Yes. Interest rates are optimized individually for each collateral type to manage risk effectively. Each collateral type has its own optimal range for safe borrowing.

***

## Can I stop using Summerstone at any time?

Absolutely. You retain full control and can revoke interest rate delegation at any moment directly from your wallet.

***

## Which Liquity V2 forks and stablecoins are supported?

We support multiple popular Liquity V2 forks and stablecoins used actively by the community. You can find the full list of supported protocols in our [Supported Protocols](/docs/borrowing/supported-protocols) section.

# Savings Calculator (https://summerstone.xyz/docs/borrowing/savings-calculator.md)

Our Return on Investment (ROI) calculator helps you determine how much you can save by using Summerstone's automated interest rate strategies. Compare the costs of manual adjustments to our automated solution and see the benefits over time.

## How the Calculator Works

The calculator compares two approaches to interest rate adjustments:

### Manual Costs

When adjusting interest rates manually, you incur two types of costs:

1. **Gas Costs:** The ETH transaction fees paid each time you adjust your rate

2. **Interest Rate Loss:** The additional interest costs from suboptimal rate adjustments

### Automated Borrowing Benefits

With Summerstone's automated borrowing, you pay a small fee but gain several benefits:

1. **Optimal Rate Adjustments:** Our solvers monitor the market continuously

2. **Zero Gas Costs:** We handle all transaction expenses

3. **MEV Protection:** Our specialized infrastructure protects your transactions

## Customization Options

You can adjust several parameters to match your specific situation:

* **Loan Size:** The principal amount of your loan (affects both service fees and potential savings)

* **Adjustment Frequency:** How often you would typically adjust rates if adjusting manually

* **Gas Price:** Expected network conditions and transaction costs

**Advanced options** allow you to fine-tune:

* **Gas Units Per Adjustment:** Complexity of your adjustment transactions

* **ETH Price:** Current market value of Ethereum

* **Interest Rate Optimization:** Estimated savings from optimal rate adjustments

* **Calculation Timeframe:** View results over 1, 2, or 5 years

## Understanding the Chart

The chart visualizes the comparison between costs and benefits over time:

* **Red Bars (Below Axis):** Service fees (costs)

* **Green Bars (Above Axis):** Gas cost savings

* **Blue Bars (Above Axis):** Interest savings from optimal rate adjustments

* **White Line:** Net value (when this crosses above zero, you achieve positive ROI)

This visualization makes it easy to see exactly when automated borrowing starts providing positive returns on your investment.

# Supported Protocols (https://summerstone.xyz/docs/borrowing/supported-protocols.md)

{/* */}

{/* */}

# MUST and Mustang (https://summerstone.xyz/docs/borrowing/supported-protocols/_must-and-mustang.md)

MUST is a USD-pegged stablecoin issued by the Mustang protocol on Saga EVM.

| Property | Value |

| --------------------------- | -------------------------------------------------------------------- |

| Protocol | Mustang ([https://must.finance](https://must.finance)) |

| Frontend | [https://app.must.finance](https://app.must.finance) |

| Stablecoin Symbol | MUST |

| Blockchain | Saga EVM |

| Chain ID | `5464` |

| Stablecoin Contract Address | `0xa8b56ce258a7f55327bde886b0e947ee059ca434` |

| Blockchain Explorer | [https://sagaevm.sagaexplorer.io/](https://sagaevm.sagaexplorer.io/) |

The information provided on this page is for informational purposes only and does not constitute financial, investment, or trading advice. Please review our [Terms of Service](/docs/borrowing/terms-of-service) before using any services described here.

## Active Strategies

# ONE and Soneta (https://summerstone.xyz/docs/borrowing/supported-protocols/_one-and-soneta.md)

ONE is a USD-pegged stablecoin issued by the Soneta protocol on Sonic.

| Property | Value |

| --------------------------- | ------------------------------------------------------------ |

| Protocol | Soneta ([https://soneta.xyz](https://soneta.xyz)) |

| Frontend | [https://www.soneta.xyz/lobby](https://www.soneta.xyz/lobby) |

| Stablecoin Symbol | ONE |

| Blockchain | Sonic |

| Chain ID | `146` |

| Stablecoin Contract Address | 0x8ed344E89527C6cE382fd1E23B4D6D4c2865b6A9 |

| Blockchain Explorer | [https://sonicscan.org](https://sonicscan.org) |

The information provided on this page is for informational purposes only and does not constitute financial, investment, or trading advice. Please review our [Terms of Service](/docs/borrowing/terms-of-service) before using any services described here.

## Active Strategies

# BOLD and Liquity V2 (https://summerstone.xyz/docs/borrowing/supported-protocols/bold-and-liquity-v2.md)

BOLD is a USD-pegged stablecoin issued by the Liquity V2 protocol on Ethereum Mainnet.

| Property | Value |

| --------------------------- | -------------------------------------------------------------------------- |

| Protocol | Liquity V2 ([https://liquity.org](https://liquity.org)) |

| Frontend | [https://liquity.app](https://liquity.app) |

| Stablecoin Symbol | BOLD |

| Blockchain | Ethereum Mainnet |

| Chain ID | `1` |

| Stablecoin Contract Address | `0x6440f144b7e50D6a8439336510312d2F54beB01D` |

| Blockchain Explorer | [https://etherscan.io](https://etherscan.io) |

| Protocol Explorer | [https://dune.com/liquity/liquity-v2](https://dune.com/liquity/liquity-v2) |

The information provided on this page is for informational purposes only and does not constitute financial, investment, or trading advice. Please review our [Terms of Service](/docs/borrowing/terms-of-service) before using any services described here.

## Active Strategies

# USND and Nerite (https://summerstone.xyz/docs/borrowing/supported-protocols/usnd-and-nerite.md)

USND is a USD-pegged stablecoin issued by the Nerite protocol on Arbitrum One.

| Property | Value |

| --------------------------- | ------------------------------------------------- |

| Protocol | Nerite ([https://nerite.org](https://nerite.org)) |

| Frontend | [https://app.nerite.org](https://app.nerite.org) |

| Stablecoin Symbol | USND |

| Blockchain | Arbitrum One |

| Chain ID | `42161` |

| Stablecoin Contract Address | `0x4ecf61a6c2fab8a047ceb3b3b263b401763e9d49` |

| Blockchain Explorer | [https://arbiscan.io](https://arbiscan.io) |

The information provided on this page is for informational purposes only and does not constitute financial, investment, or trading advice. Please review our [Terms of Service](/docs/borrowing/terms-of-service) before using any services described here.

## Active Strategies

# Terms of Service (https://summerstone.xyz/docs/borrowing/terms-of-service.md)

These Terms of Service (the "Terms") explain what happens when you appoint us as your **non‑custodial rate automation provider** (the "Service"). You do that by setting our delegate address for your loan(s) on one or more independent lending protocols ("Core Protocols"). If you do not agree to these Terms, do not set that delegation.

## 1. Who may use the Service

* You are at least 18 years old and legally able to make contracts.

* You follow the laws of your country. If local rules ban blockchain borrowing tools, do not use the Service.

## 2. What we do - and **don't** do

* **Delegate only.** Using your own wallet, you give our address limited authority to automate the interest‑rate settings of your loan. Nothing more.

* **No custody.** We never hold your assets or private keys. The Core Protocols still hold collateral and debt. You can revoke our delegation at any time with your wallet.

* **No control over Core Protocols.** We did not build them, cannot fix them, and cannot stop unexpected behavior.

* **No guarantees or advice.** We do not promise to lower your rate, prevent liquidation, or achieve any outcome. Nothing we say is financial, legal, tax, or trading advice.

* **Off‑chain actions.** After delegation, our off-chain systems may act on your behalf within the constraints defined. We are **not obliged** to act, and any action may be skipped, delayed, or fail.

* **Not a regulated entity.** We are not a bank, broker, exchange, or money‑service business, and we are not regulated as one.

## 3. Big risks you accept

1. **Protocol bugs or hacks.** Core Protocols can fail or be exploited; our off‑chain systems may also malfunction.

2. **Interest‑rate swings.** Rates can spike suddenly, and our solvers might not react in time - or at all.

3. **Liquidations.** Falling collateral value can trigger automatic liquidations, irrespective of your interest rate.

4. **Network congestion.** High gas fees or chain delays can stop us from acting when needed.

5. **Regulatory changes.** Laws can change and make it hard or illegal for you to repay or keep using blockchain tools.

## 4. Your responsibilities

* **Maintain collateral.** You are responsible for monitoring collateral levels and adding more if needed.

* **Stay legal.** Do not use the Service for money laundering, sanctions evasion, or any crime.

* **Understand the rules.** Read how our delegate operates before you enable it.

* **Indemnity.** If someone sues us because of something you did, you will cover our costs (including lawyers' fees).

## 5. No promises ("As Is")

The Service is provided **"as is" and "as available."** We make **no warranty** - not for uptime, accuracy, security, or any result. We may miss triggers, execute late, or fail completely. You accept that risk.

## 6. Limits of liability

To the fullest extent allowed by law:

* We are **not** responsible for any indirect, special, or consequential loss; lost profits; lost data; or loss of goodwill.

* If we are found liable anyway, our total liability is capped at **US $1.00**.

## 7. Stopping or changing the Service

We may upgrade, pause, or shut down our off‑chain systems or resign our delegate address without notice. You can revoke delegation at any time.

## 8. Disputes

* **Informal resolution first.** Contact us; we will try to resolve any issue in good faith.

* **Arbitration.** If we cannot settle it informally within 30 days, any dispute will be resolved individually and confidentially by binding arbitration under widely accepted international rules. The arbitrator's decision is final and enforceable.

* **No class actions.** You and we may bring claims only on our own behalf, not as part of a class, collective, or representative action.

## 9. Updates to these Terms

We may update these Terms by publishing a new version at any time. Using the Service after the update means you accept the new Terms.

**By delegating interest rate automation to our address, you confirm that you have read, understood, and agreed to these Terms, and that you accept all risks described above.**

# Why Automate Your Interest Rate? (https://summerstone.xyz/docs/borrowing/why-automate-your-interest-rate.md)

Automating interest rate adjustments maximizes your capital efficiency and significantly reduces redemption risks and costs:

* **Zero Gas Fees:** All adjustment-related gas costs are covered by us.

* **Optimal Rates:** Real-time market monitoring ensures adjustments are executed precisely and timely.

* **Proactive Adjustments:** Risk of redemptions is actively minimized through proactive adjustments.

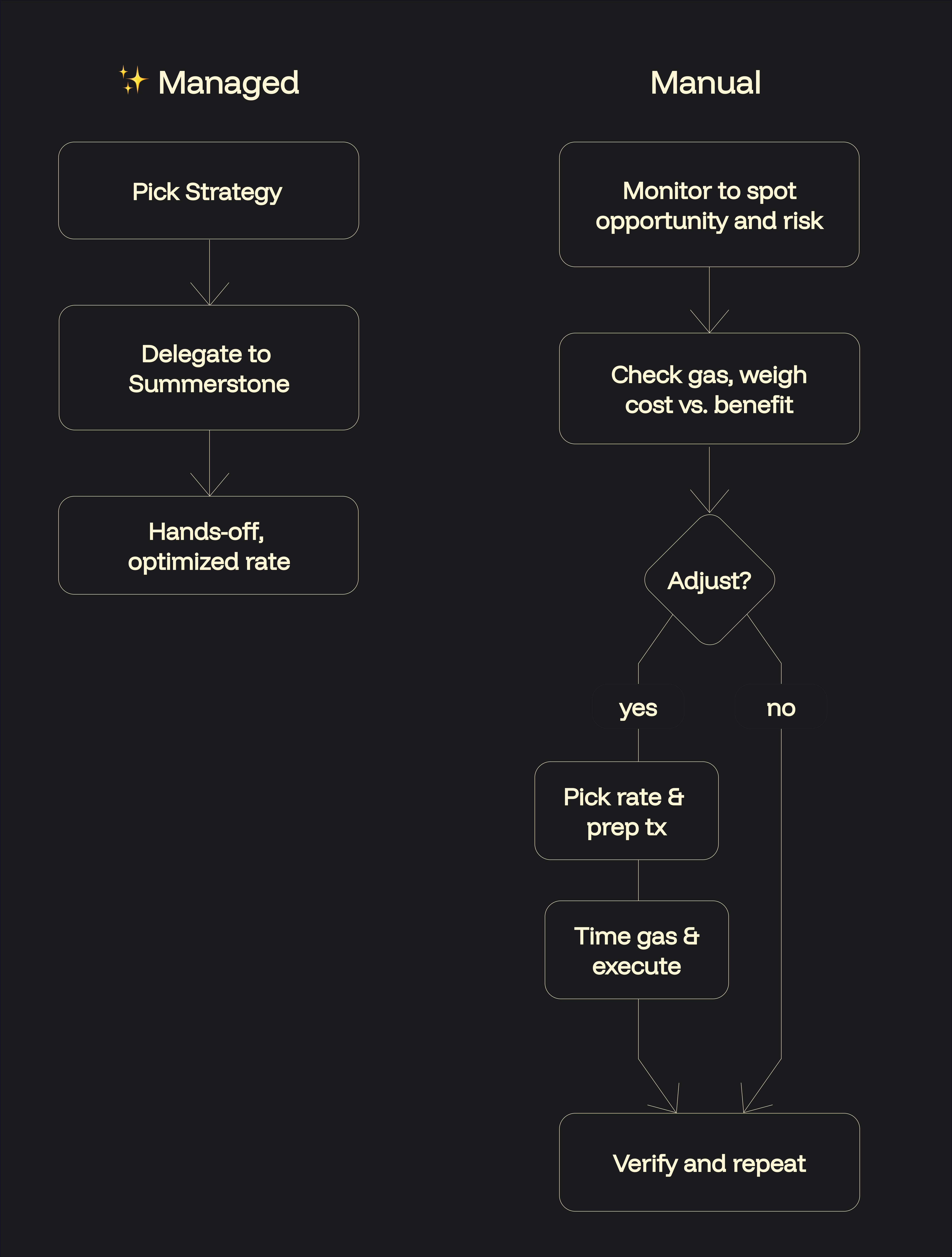

## Manual vs. Automated

The following diagram compares Summerstone's automated approach to manual adjustments:

### Explanation of the Diagram:

* **Delegation:** You delegate authority to adjust your loan’s interest rate (no fund custody involved).

* **Monitoring:** Our algorithm constantly evaluates market conditions, including debt positions, redemption risks, and gas conditions.

* **Adjustment Calculation:** The solver computes the optimal interest rate adjustments based on your preset risk strategy.

* **Execution:** Adjustments are securely executed directly on the Liquity V2 protocol, reflected transparently onchain.

## Getting Started:

1. Open your loan settings in a supported frontend of your chosen protocol.

2. Delegate interest rate automation to our verified address. Check our [supported protocols](/docs/borrowing/supported-protocols).

3. Confirm the transaction - your loans are now fully automated.

# Frequently Asked Questions (FAQs) (https://summerstone.xyz/docs/borrowing/frequently-asked-questions.md)

## What exactly does Summerstone do?

Summerstone provides automated interest rate adjustments for your Liquity V2-based loans. By continuously monitoring market conditions, our system optimally adjusts your interest rate to keep borrowing costs low, proactively minimize redemption risk, and eliminate the hassle of manual adjustments.

***

## How do automated interest rate adjustments work?

Our system monitors key metrics continuously, including:

* Redemption risk and debt positions

* Market price fluctuations

* Network gas conditions

* Liquity protocol status and events

Based on these metrics, our algorithms determine precisely when and how to adjust your loan's interest rate, optimizing your borrowing efficiency.

***

## How much does Summerstone cost?

We charge a straightforward 0.3% annual service fee based on your total loan amount, enforced transparently by the protocol. For most users, these costs are offset by:

* Reduced gas expenses from eliminating manual adjustments

* Lower average interest rates

* Reduced risk of redemption penalties

You can calculate your exact potential savings using our [Savings Calculator](/docs/borrowing/savings-calculator).

***

## Is delegating interest rate adjustments secure?

Yes. Delegation through Liquity V2 protocols is inherently safe and limited:

* Delegates / batch managers **only** have the ability to adjust interest rates.

* Delegates / batch managers **cannot** access or transfer your funds or modify other loan parameters.

* Delegation permissions and boundaries are verifiable directly onchain.

***

## Can Summerstone guarantee protection against redemptions?

While our automated system significantly reduces the likelihood of redemption by proactively adjusting rates, we cannot guarantee complete protection due to inherent market volatility and liquidity factors.

Please review our comprehensive [Terms of Service](/docs/borrowing/terms-of-service) to understand these risks fully.

***

## Which frontends can I use?

Liquity does not run its own frontend. You can use any frontend that supports interest rate delegation for Liquity V2 protocols. You can find independent frontends [here](https://www.liquity.org/frontend-v2) or just head to [liquity.app](https://liquity.app/).

***

## How frequently are interest rates adjusted?

Adjustments typically happen at most once per week under normal conditions. During high-risk periods, adjustments may occur more frequently as needed, within the limits enforced by the Liquity protocol.

***

## Do rates differ based on collateral types?

Yes. Interest rates are optimized individually for each collateral type to manage risk effectively. Each collateral type has its own optimal range for safe borrowing.

***

## Can I stop using Summerstone at any time?

Absolutely. You retain full control and can revoke interest rate delegation at any moment directly from your wallet.

***

## Which Liquity V2 forks and stablecoins are supported?

We support multiple popular Liquity V2 forks and stablecoins used actively by the community. You can find the full list of supported protocols in our [Supported Protocols](/docs/borrowing/supported-protocols) section.

# Savings Calculator (https://summerstone.xyz/docs/borrowing/savings-calculator.md)

Our Return on Investment (ROI) calculator helps you determine how much you can save by using Summerstone's automated interest rate strategies. Compare the costs of manual adjustments to our automated solution and see the benefits over time.

## How the Calculator Works

The calculator compares two approaches to interest rate adjustments:

### Manual Costs

When adjusting interest rates manually, you incur two types of costs:

1. **Gas Costs:** The ETH transaction fees paid each time you adjust your rate

2. **Interest Rate Loss:** The additional interest costs from suboptimal rate adjustments

### Automated Borrowing Benefits

With Summerstone's automated borrowing, you pay a small fee but gain several benefits:

1. **Optimal Rate Adjustments:** Our solvers monitor the market continuously

2. **Zero Gas Costs:** We handle all transaction expenses

3. **MEV Protection:** Our specialized infrastructure protects your transactions

## Customization Options

You can adjust several parameters to match your specific situation:

* **Loan Size:** The principal amount of your loan (affects both service fees and potential savings)

* **Adjustment Frequency:** How often you would typically adjust rates if adjusting manually

* **Gas Price:** Expected network conditions and transaction costs

**Advanced options** allow you to fine-tune:

* **Gas Units Per Adjustment:** Complexity of your adjustment transactions

* **ETH Price:** Current market value of Ethereum

* **Interest Rate Optimization:** Estimated savings from optimal rate adjustments

* **Calculation Timeframe:** View results over 1, 2, or 5 years

## Understanding the Chart

The chart visualizes the comparison between costs and benefits over time:

* **Red Bars (Below Axis):** Service fees (costs)

* **Green Bars (Above Axis):** Gas cost savings

* **Blue Bars (Above Axis):** Interest savings from optimal rate adjustments

* **White Line:** Net value (when this crosses above zero, you achieve positive ROI)

This visualization makes it easy to see exactly when automated borrowing starts providing positive returns on your investment.

# Supported Protocols (https://summerstone.xyz/docs/borrowing/supported-protocols.md)

{/* */}

{/* */}

# MUST and Mustang (https://summerstone.xyz/docs/borrowing/supported-protocols/_must-and-mustang.md)

MUST is a USD-pegged stablecoin issued by the Mustang protocol on Saga EVM.

| Property | Value |

| --------------------------- | -------------------------------------------------------------------- |

| Protocol | Mustang ([https://must.finance](https://must.finance)) |

| Frontend | [https://app.must.finance](https://app.must.finance) |

| Stablecoin Symbol | MUST |

| Blockchain | Saga EVM |

| Chain ID | `5464` |

| Stablecoin Contract Address | `0xa8b56ce258a7f55327bde886b0e947ee059ca434` |

| Blockchain Explorer | [https://sagaevm.sagaexplorer.io/](https://sagaevm.sagaexplorer.io/) |

The information provided on this page is for informational purposes only and does not constitute financial, investment, or trading advice. Please review our [Terms of Service](/docs/borrowing/terms-of-service) before using any services described here.

## Active Strategies

# ONE and Soneta (https://summerstone.xyz/docs/borrowing/supported-protocols/_one-and-soneta.md)

ONE is a USD-pegged stablecoin issued by the Soneta protocol on Sonic.

| Property | Value |

| --------------------------- | ------------------------------------------------------------ |

| Protocol | Soneta ([https://soneta.xyz](https://soneta.xyz)) |

| Frontend | [https://www.soneta.xyz/lobby](https://www.soneta.xyz/lobby) |

| Stablecoin Symbol | ONE |

| Blockchain | Sonic |

| Chain ID | `146` |

| Stablecoin Contract Address | 0x8ed344E89527C6cE382fd1E23B4D6D4c2865b6A9 |

| Blockchain Explorer | [https://sonicscan.org](https://sonicscan.org) |

The information provided on this page is for informational purposes only and does not constitute financial, investment, or trading advice. Please review our [Terms of Service](/docs/borrowing/terms-of-service) before using any services described here.

## Active Strategies

# BOLD and Liquity V2 (https://summerstone.xyz/docs/borrowing/supported-protocols/bold-and-liquity-v2.md)

BOLD is a USD-pegged stablecoin issued by the Liquity V2 protocol on Ethereum Mainnet.

| Property | Value |

| --------------------------- | -------------------------------------------------------------------------- |

| Protocol | Liquity V2 ([https://liquity.org](https://liquity.org)) |

| Frontend | [https://liquity.app](https://liquity.app) |

| Stablecoin Symbol | BOLD |

| Blockchain | Ethereum Mainnet |

| Chain ID | `1` |

| Stablecoin Contract Address | `0x6440f144b7e50D6a8439336510312d2F54beB01D` |

| Blockchain Explorer | [https://etherscan.io](https://etherscan.io) |

| Protocol Explorer | [https://dune.com/liquity/liquity-v2](https://dune.com/liquity/liquity-v2) |

The information provided on this page is for informational purposes only and does not constitute financial, investment, or trading advice. Please review our [Terms of Service](/docs/borrowing/terms-of-service) before using any services described here.

## Active Strategies

# USND and Nerite (https://summerstone.xyz/docs/borrowing/supported-protocols/usnd-and-nerite.md)

USND is a USD-pegged stablecoin issued by the Nerite protocol on Arbitrum One.

| Property | Value |

| --------------------------- | ------------------------------------------------- |

| Protocol | Nerite ([https://nerite.org](https://nerite.org)) |

| Frontend | [https://app.nerite.org](https://app.nerite.org) |

| Stablecoin Symbol | USND |

| Blockchain | Arbitrum One |

| Chain ID | `42161` |

| Stablecoin Contract Address | `0x4ecf61a6c2fab8a047ceb3b3b263b401763e9d49` |

| Blockchain Explorer | [https://arbiscan.io](https://arbiscan.io) |

The information provided on this page is for informational purposes only and does not constitute financial, investment, or trading advice. Please review our [Terms of Service](/docs/borrowing/terms-of-service) before using any services described here.

## Active Strategies

# Terms of Service (https://summerstone.xyz/docs/borrowing/terms-of-service.md)

These Terms of Service (the "Terms") explain what happens when you appoint us as your **non‑custodial rate automation provider** (the "Service"). You do that by setting our delegate address for your loan(s) on one or more independent lending protocols ("Core Protocols"). If you do not agree to these Terms, do not set that delegation.

## 1. Who may use the Service

* You are at least 18 years old and legally able to make contracts.

* You follow the laws of your country. If local rules ban blockchain borrowing tools, do not use the Service.

## 2. What we do - and **don't** do

* **Delegate only.** Using your own wallet, you give our address limited authority to automate the interest‑rate settings of your loan. Nothing more.

* **No custody.** We never hold your assets or private keys. The Core Protocols still hold collateral and debt. You can revoke our delegation at any time with your wallet.

* **No control over Core Protocols.** We did not build them, cannot fix them, and cannot stop unexpected behavior.

* **No guarantees or advice.** We do not promise to lower your rate, prevent liquidation, or achieve any outcome. Nothing we say is financial, legal, tax, or trading advice.

* **Off‑chain actions.** After delegation, our off-chain systems may act on your behalf within the constraints defined. We are **not obliged** to act, and any action may be skipped, delayed, or fail.

* **Not a regulated entity.** We are not a bank, broker, exchange, or money‑service business, and we are not regulated as one.

## 3. Big risks you accept

1. **Protocol bugs or hacks.** Core Protocols can fail or be exploited; our off‑chain systems may also malfunction.

2. **Interest‑rate swings.** Rates can spike suddenly, and our solvers might not react in time - or at all.

3. **Liquidations.** Falling collateral value can trigger automatic liquidations, irrespective of your interest rate.

4. **Network congestion.** High gas fees or chain delays can stop us from acting when needed.

5. **Regulatory changes.** Laws can change and make it hard or illegal for you to repay or keep using blockchain tools.

## 4. Your responsibilities

* **Maintain collateral.** You are responsible for monitoring collateral levels and adding more if needed.

* **Stay legal.** Do not use the Service for money laundering, sanctions evasion, or any crime.

* **Understand the rules.** Read how our delegate operates before you enable it.

* **Indemnity.** If someone sues us because of something you did, you will cover our costs (including lawyers' fees).

## 5. No promises ("As Is")

The Service is provided **"as is" and "as available."** We make **no warranty** - not for uptime, accuracy, security, or any result. We may miss triggers, execute late, or fail completely. You accept that risk.

## 6. Limits of liability

To the fullest extent allowed by law:

* We are **not** responsible for any indirect, special, or consequential loss; lost profits; lost data; or loss of goodwill.

* If we are found liable anyway, our total liability is capped at **US $1.00**.

## 7. Stopping or changing the Service

We may upgrade, pause, or shut down our off‑chain systems or resign our delegate address without notice. You can revoke delegation at any time.

## 8. Disputes

* **Informal resolution first.** Contact us; we will try to resolve any issue in good faith.

* **Arbitration.** If we cannot settle it informally within 30 days, any dispute will be resolved individually and confidentially by binding arbitration under widely accepted international rules. The arbitrator's decision is final and enforceable.

* **No class actions.** You and we may bring claims only on our own behalf, not as part of a class, collective, or representative action.

## 9. Updates to these Terms

We may update these Terms by publishing a new version at any time. Using the Service after the update means you accept the new Terms.

**By delegating interest rate automation to our address, you confirm that you have read, understood, and agreed to these Terms, and that you accept all risks described above.**

# Why Automate Your Interest Rate? (https://summerstone.xyz/docs/borrowing/why-automate-your-interest-rate.md)

Automating interest rate adjustments maximizes your capital efficiency and significantly reduces redemption risks and costs:

* **Zero Gas Fees:** All adjustment-related gas costs are covered by us.

* **Optimal Rates:** Real-time market monitoring ensures adjustments are executed precisely and timely.

* **Proactive Adjustments:** Risk of redemptions is actively minimized through proactive adjustments.

## Manual vs. Automated

The following diagram compares Summerstone's automated approach to manual adjustments:

## Manual Adjustments: Hidden Costs and Risks

Adjusting your own interest rates may seem straightforward, but often involves significant unseen costs:

* **Gas Fees:** Frequent manual adjustments become costly quickly.

* **Redemption Risk:** Manual updates are often too late or suboptimal, increasing the risk of loan redemption.

* **Emotional Cost:** Constant anxiety and stressful emergency adjustments during market volatility.

* **Capital Inefficiency:** Overpaying interest due to delayed or missed adjustments.

## **Why Summerstone Rate Automation?**

Summerstone's automated interest rate strategies eliminate the burden of costs associated with manual adjustments, maximizing your capital efficiency and significantly reducing redemption risks:

* **Significant savings:** Automatically optimized interest rates can significantly lower your borrowing costs compared to manual adjustments.

* **Reduced gas costs to zero:** Automated adjustments save significant gas costs compared to frequent manual adjustments.

* **Optimized Interest Rates:** Our continuous monitoring and real-time adjustments lead to lower average interest rates. Manual updates are often too late or suboptimal, increasing costs and the risk of loan redemption.

* **Proactive risk reduction:** Our algorithm monitors market conditions around the clock, actively reducing user’s redemption risk.

* **User remains in control:** Delegate only the automation of your interest rate. Summerstone can never take custody or control of your funds.

* **Trusted expertise:** As long-term partners of Liquity AG, we leverage deep expertise in blockchain analytics and operational excellence.

# Summerstone Brand Kit (https://summerstone.xyz/docs/brand-kit.md)

This section includes logos, wordmarks, colors and fonts.

## Brand Colors

* **Carrot orange**: #FA970B

* **Eerie black**: #222020

* **Corn silk**: #FEF6D5

## Fonts

* **Titles**: Funnel Display

* **Content**: Funnel Sans

## Download our Brand Kit

Download the [Summerstone Brand Kit](/files/Summerstone_Brand_Kit.zip).

# Blog (https://summerstone.xyz/blog.md)

Announcements and updates from the Summerstone team.

## Posts

- [Summerstone extends rate automation to Mustang](https://summerstone.xyz/blog/summerstone-and-mustang.md): Summerstone is extending rate automation services to Saga's native stablecoin MUST.

- [Summerstone partners with Nerite](https://summerstone.xyz/blog/summerstone-and-nerite.md): As part of our wider commitment to the Liquity ecosystem, Summerstone is partnering with Nerite to make the future of borrowing a reality on Arbitrum One.

# Summerstone extends rate automation to Mustang (https://summerstone.xyz/blog/summerstone-and-mustang.md)

Summerstone is extending rate automation services to Saga's native stablecoin MUST.

## Mustang Finance & MUST, built for Saga

Mustang Finance is bringing [Liquity V2](https://liquity.org/)-based borrowing to Saga EVM. Through the CDP, Saga users can mint the stablecoin MUST, with a rock-solid USD peg.

The MUST stablecoin can be minted by depositing one of seven types of collateral: WETH, yETH, tBTC, wSAGA, wstAtom, KING and yUSD. Once deposited, users can open a trove setting their own interest rates without relying on governance or on any specific algorithm.

## Manual Adjustments: Hidden Costs and Risks

Adjusting your own interest rates may seem straightforward, but often involves significant unseen costs:

* **Gas Fees:** Frequent manual adjustments become costly quickly.

* **Redemption Risk:** Manual updates are often too late or suboptimal, increasing the risk of loan redemption.

* **Emotional Cost:** Constant anxiety and stressful emergency adjustments during market volatility.

* **Capital Inefficiency:** Overpaying interest due to delayed or missed adjustments.

## **Why Summerstone Rate Automation?**

Summerstone's automated interest rate strategies eliminate the burden of costs associated with manual adjustments, maximizing your capital efficiency and significantly reducing redemption risks:

* **Significant savings:** Automatically optimized interest rates can significantly lower your borrowing costs compared to manual adjustments.

* **Reduced gas costs to zero:** Automated adjustments save significant gas costs compared to frequent manual adjustments.

* **Optimized Interest Rates:** Our continuous monitoring and real-time adjustments lead to lower average interest rates. Manual updates are often too late or suboptimal, increasing costs and the risk of loan redemption.

* **Proactive risk reduction:** Our algorithm monitors market conditions around the clock, actively reducing user’s redemption risk.

* **User remains in control:** Delegate only the automation of your interest rate. Summerstone can never take custody or control of your funds.

* **Trusted expertise:** As long-term partners of Liquity AG, we leverage deep expertise in blockchain analytics and operational excellence.

# Summerstone Brand Kit (https://summerstone.xyz/docs/brand-kit.md)

This section includes logos, wordmarks, colors and fonts.

## Brand Colors

* **Carrot orange**: #FA970B

* **Eerie black**: #222020

* **Corn silk**: #FEF6D5

## Fonts

* **Titles**: Funnel Display

* **Content**: Funnel Sans

## Download our Brand Kit

Download the [Summerstone Brand Kit](/files/Summerstone_Brand_Kit.zip).

# Blog (https://summerstone.xyz/blog.md)

Announcements and updates from the Summerstone team.

## Posts

- [Summerstone extends rate automation to Mustang](https://summerstone.xyz/blog/summerstone-and-mustang.md): Summerstone is extending rate automation services to Saga's native stablecoin MUST.

- [Summerstone partners with Nerite](https://summerstone.xyz/blog/summerstone-and-nerite.md): As part of our wider commitment to the Liquity ecosystem, Summerstone is partnering with Nerite to make the future of borrowing a reality on Arbitrum One.

# Summerstone extends rate automation to Mustang (https://summerstone.xyz/blog/summerstone-and-mustang.md)

Summerstone is extending rate automation services to Saga's native stablecoin MUST.

## Mustang Finance & MUST, built for Saga

Mustang Finance is bringing [Liquity V2](https://liquity.org/)-based borrowing to Saga EVM. Through the CDP, Saga users can mint the stablecoin MUST, with a rock-solid USD peg.

The MUST stablecoin can be minted by depositing one of seven types of collateral: WETH, yETH, tBTC, wSAGA, wstAtom, KING and yUSD. Once deposited, users can open a trove setting their own interest rates without relying on governance or on any specific algorithm.

## How can Saga Users Benefit from Summerstone

Summerstone aligns with user's, reducing their overall borrowing costs through calculating precise, reliable rates.

We do so by:

→ **24/7 monitoring:** Our solvers monitor all troves, system parameters, market conditions and outside debt to have a holistic view of the system's status.

→ **Optimized rate tuning**: We spread out the amount of changes and keep borrowing costs as low as possible while protecting against redemptions, the automatic peg-stabilization mechanism used by Mustang Finance.

At any point, our solvers are prepared to trigger rate adjustments of our automated troves.

## Get started using Summerstone interest rate strategies on Mustang

1. Head to [app.must.finance](https://apps.must.finance/) and connect your wallet.

2. Pick your collateral, and amount to borrow.

3. Set your interest rate as "Delegated" and pick the Strategy Delegate Address of your chosen collateral from the [Summerstone Docs](https://summerstone.xyz/docs/borrowing/supported-protocols/must-and-mustang).

Alternatively, you can try out the [Summerstone Wizard 🧙♂️](https://ir-wizard.summerstone.xyz/): a new interface to delegate rate automation of your Liquity-based loans. All in one place. We currently support Liquity, Mustang Finance, Nerite, Soneta.

Read more about Mustang on [docs.must.finance](https://docs.must.finance/)

# Summerstone partners with Nerite (https://summerstone.xyz/blog/summerstone-and-nerite.md)

As part of our wider commitment to the Liquity ecosystem, Summerstone is partnering with Nerite to make the future of borrowing a reality on Arbitrum One.

## Nerite & USND, built specifically for Arbitrum

[Nerite](https://nerite.org/) is a [Liquity V2](https://liquity.org/)-based borrowing protocol. It inherits the protocol’s immutability while letting users mint USND, Nerite’s native USD-pegged stablecoin.

In Nerite, borrowers can establish their own interest rates, according to what they are willing to pay without relying on governance or a protocol-set algorithm rates.

### Nerite expands Liquity’s model

→ **Broader collateral:** In addition to ETH, wstETH, and rETH, Nerite accepts rsETH, weETH, ARB, COMP, and tBTC.

→ **Streamable stablecoin**: USND, is issued as a [Superfluid super token](https://docs.superfluid.org/docs/concepts/superfluid#super-tokens), allowing value to flow continuously rather than by discrete transfers.

→ **Lower entry:** Minimum debt per borrow on Nerite is 500 USND, one quarter the Liquity V2 baseline, opening the door to smaller positions.

## Powering market operations for Nerite

Market operations becomes increasingly important to guarantee the stability of USD-pegged tokens, especially when backed by diverse sets of liquid staking derivatives and non ETH assets.

Summerstone will continuously map Nerite’s market conditions. Powered by real time data, Summerstone’s interest rate solvers and liquidation engine are prepared to trigger interest rate adjustments and precise liquidations across every supported collateral, adapting to each specific liquidity profile and volatility.

As with Liquity V2, Nerite borrowers will be able to delegate their interest rate automation to Summerstone.

### How this benefits users

→ **Reliable rates.** Interest bands tuned for market depth rather than rough averages with reliable data.

→ **Predictable peg behaviour**, creating the basis for a sustainable market.

→ **Trusted Manager.** Users can delegate changes to their interest rates to a long-standing, reputable member of the Liquity and Nerite ecosystems.

## Get Started

Nerite opens the door to user-set interest rates on Arbitrum. Summerstone supplies rate engineering, and data monitoring. By working side-by-side, we aim to set a new standard for self-custodial borrowing on Arbiturm.

Get started on [nerite.org](https://nerite.org/)

To get in touch, [reach out to us](https://graphops.notion.site/32e2931a55f7814bbea2edfe9481579d?pvs=105).

# Research (https://summerstone.xyz/research.md)

Research and publications from the Summerstone team.

## Posts

- [Pendle as Yield Infrastructure](https://summerstone.xyz/research/pendle.md): How the venue works, and how lending protocols shape its markets.

- [Morpho curators: market structure in 2025](https://summerstone.xyz/research/morpho-curators-market-structure-january-2026.md): A look into liquidity, curator consolidation, their supply, and the stablecoin landscape in Morpho.

- [Liquity V2 Batch Managers: ICP-Based vs Summerstone](https://summerstone.xyz/research/liquity-v2-rate-managers.md): This article outlines how ICP-based batch managers differ from Summerstone's approach.

# Pendle as Yield Infrastructure (https://summerstone.xyz/research/pendle.md)

How the venue works, and how lending protocols shape its markets.

## Summary

In 2025, Pendle shifted from a general yield-tokenization protocol into infrastructure for locking stablecoin yields at fixed rates. ETH derivatives, once Pendle's core use case, declined to just 2.9% of open interest. Activity consolidated around a narrow set of stablecoin instruments where implied rates trade persistently at 8–20%, well above ETH derivative yields of 3–7%.

Users overwhelmingly buy and hold. 85.6% of capital stays until maturity, 98.9% of wallets never sell, and only 7.4% of expired capital rolls into the next expiry. Pendle operates as a one-way funding lock rather than a trading venue.

But this capital doesn't arrive directly. 73.8% of Pendle's external PT open interest flows through lending protocol intermediaries: Aave V3 alone holds 54.7% across 26 vault contracts. The dominant strategy is looping yield-bearing stablecoins: deposit into Pendle, post PT as collateral on a lending venue, borrow stablecoins, re-enter Pendle. This makes Pendle's scale inseparable from the lending venues that consume its output, and inflates headline open interest.

### Key findings:

* $538M in active PT open interest, with 96.1% in stablecoins.

* About 66-day weighted average duration: the average dollar on Pendle is exposed to rate moves for roughly two months. Pendle is short-duration yield infrastructure, not a term funding venue.

* 93% of dollar-denominated OI in holding-behavior markets: positions are sticky, not churning.

* 54.7% of all PT units are held by Aave V3: Pendle is an intermediary-consumed infrastructure and integrated directly with lending venues, not a direct-to-user venue.

* We estimate 10–31% of OI is leverage-generated rather than independently committed capital.

* Only 7.4% of expired capital rolls into the next expiry. When PT positions expire without rollover, the associated lending positions (loops, collateral commitments) must also unwind, creating periodic deleveraging pressure across the lending venues that warehouse PT.

* 66.1% of outstanding YT sits with addresses that only ever minted (PT-motivated), while just 15.5% represents independent yield-long demand. The yield side of Pendle is largely a byproduct of principal token manufacturing, not the primary product.

## What Pendle Is

Pendle is infrastructure for separating, pricing, and transferring future yield. It tokenizes yield that originates elsewhere. Pendle takes yield-bearing assets and splits them into their principal and yield components, each tradeable independently through a dedicated AMM. Through the venue participants can lock fixed rates, trade yield exposure, or hold positions until maturity.

The mechanism begins with [Standardized Yield (SY)](https://docs.pendle.finance/pendle-v2/ProtocolMechanics/YieldTokenization/SY), a token wrapper conforming to [EIP-5115](https://eips.ethereum.org/EIPS/eip-5115) that provides a common interface for any yield-bearing asset and standardizes how Pendle interacts with the full range of yield-bearing assets across DeFi. When a token is deposited into Pendle, it is first wrapped into its SY representation (e.g., sUSDe becomes SY-sUSDe).

SY is then split into two tokens in equal quantities: a Principal Token (PT) and a Yield Token (YT). The split is atomic: 1 SY always produces 1 PT and 1 YT, and the [two cannot be created independently.](https://docs.pendle.finance/pendle-v2/Developers/HighLevelArchitecture)

* A [Principal Token](https://docs.pendle.finance/pendle-v2/ProtocolMechanics/YieldTokenization/PT) is a claim on the underlying principal at maturity. PT trades at a discount to its underlying asset, and that discount narrows as maturity approaches, converging toward par at expiry. This predictable price path is what makes PT function as collateral on external lending venues, a dynamic central to how Pendle's open interest is consumed downstream.

* A [Yield Token](https://docs.pendle.finance/pendle-v2/ProtocolMechanics/YieldTokenization/YT) is a claim on all yield generated by the underlying from the point of acquisition until maturity. YT holders can claim accrued yield at any time. At expiry, YT's value converges to zero: whatever yield was generated has been captured, and the token carries no residual claim. After maturity, only PT is required to redeem the underlying.

Each underlying asset can support multiple Pendle markets at different maturities, each with its own liquidity pool and its own implied rate. Trading occurs through a single PT/SY liquidity pool per market. The [AMM is time-aware](https://docs.pendle.finance/pendle-v2/ProtocolMechanics/LiquidityEngines/AMM): its curve shifts to account for PT's natural price appreciation as maturity approaches, concentrating liquidity around expected yield ranges and reducing impermanent loss for liquidity providers. YT trades route through the same pool via flash swaps. A single pool serves both sides of the yield split.

## SY-Notional in 2025: Activity & Composition

SY-notional captures the priced economic throughput flowing through Pendle's V3 markets: the daily volume of Standardized Yield tokens repriced via the AMM, representing how much yield exposure changes hands.

* For most of 2025, daily swaps ranged 500–2,000 with trader counts tracking closely. Activity spiked sharply in early November: daily swaps exceeded [9,400 and unique traders hit 8,000.](https://dune.com/queries/6523115/10329644)

* Late-2025 throughput was dominated by [Hyperlend](https://dune.com/queries/6530486/10329737), [Ethena (USDe/sUSDe), Resolv, Open Dollar](https://dune.com/queries/6546841/10350401) – almost entirely stablecoin-sourced. ETH-derivative swap activity concentrated in H1 2025 and became minimal after June.

### ETH-Derivative Throughput

SY-notional across a whitelist of ETH-derivative underlyings (weETH, pufETH, rsETH, rswETH, tETH) shows extreme sparsity punctuated by episodic spikes.

[Q1 throughput totaled $90.4M, growing to $116.1M in Q2 before collapsing post-June to $16.2M in Q3](https://dune.com/queries/6529731/10329443). The decline is more severe than USD figures suggest: ETH rallied from \~$2,800 to a $4,900 ATH in late August, meaning constant activity levels would have produced *higher* Q3 volumes, not lower. The USD-denominated drop understates the real contraction in ETH-notional terms.

PT-notional for the same ETH-derivatives shows expiry-driven spikes in late May and June, likely tied to duration compression and roll/unwind events. Outside these episodes, PT-notional is minimal, consistent with steady-state rolling rather than active rate trading.

## Open Interest

Open interest measures total Principal Tokens outstanding: capital committed to fixed-rate positions that hasn't expired or been redeemed. Where SY-notional and PT-notional measure flow (what passed through), OI measures stock (what stayed).

Three lenses apply: PT OI in units (principal committed), PT OI in USD (dollar value of commitments, requiring pricing), and duration outstanding (PT OI × time-to-maturity, yielding rate-dollar-years of risk in the system).

### Unit-Denominated Open Interest: Scale & Concentration

**Scale & Concentration**

Aggregate active PT OI stands at [538M units across 96 unexpired markets](https://dune.com/queries/6569097/10378004). Concentration of current active markets is extreme: the [top 5 markets hold 80% of OI, the top 10 hold 95%](https://dune.com/queries/6569097/10378004).

The [leading markets](https://dune.com/queries/6569097/10378004) (PT-sUSDe-7MAY2026 (41.8%), PT-srUSDe-2APR2026 (15.4%), PT-sNUSD-5MAR2026 (13.8%)) reflect the current expiry cycle with asset concentration around the Ethena ecosystem and Strata's yield products (sUSDe, srUSDe, USDe, sENA, jrUSDe collectively \~65% of active OI).

This is contingent on current market preferences in this particular window of time and could shift with subsequent expiry cycles. Active markets vary greatly as throughout compiling this report some have expired.

**Temporal Concentration**

Temporal concentration in Pendle markets is structural, reflecting how yield markets work:

* Lifecycle accumulation: older markets have had more time to build OI

* Capital efficiency: traders prefer shorter lockups

* Price certainty: PT converges to par at expiry

* Roll behavior: traders exit and roll into next maturity

Unlike asset concentration (which is contingent), the preference for sub-90-day maturities is structural: PT buyers prefer shorter duration locks for capital efficiency and price certainty (PT converges to par at expiry, reducing mark-to-market risk).

The bulk of active OI sits in the 30–90 day bucket (58%), followed by 0–30 days (14.4%). The 180+ day bucket is essentially empty. This mid-curve concentration reflects the current expiry calendar: the March through May 2026 cluster carries the majority of commitments.

**Asset Composition**

* Stablecoin dominance is total across all buckets. ETH-derivative categories (eETH, stETH, Other ETH) are essentially minimal beyond the 0-30 day bucket.

* Different stablecoins [dominate different parts of the curve](https://dune.com/queries/6571180/10380702):

* 0–30 days: NUSD (Neutrl) at 92.9%, reflecting near-term maturity concentration in a single issuer

* 30–90 days: Ethena ecosystem at 97.7% (USDe variants 90.9% and other non-stablecoin assets like sENA 6.9%), representing the core of Pendle's current OI.

* 90–180 days: cUSD (Cap) at 57.7%, with a broader mix including other USD-denominated positions (28.8%) and a smaller Ethena share (6.9%)

### Dollar denominated PT Open Interest

Pricing PT open interest quantifies warehoused funding commitments on Pendle in economic terms. Active dollar-denominated OI stands at $538M across 45 priced markets.

* [Stablecoins account for 96.1% ($517M), ETH derivatives 2.9% ($15.7M), and other assets 1.0%.](https://dune.com/queries/6681180/10522583) The stablecoin dominance observed in unit terms carries through to dollar terms without distortion

* The pricing confidence breakdown for stablecoins: [47% carries direct observable swap prices, 16% relies on the $1 peg assumption, and 37% uses manual estimates](https://dune.com/queries/6681180/10522583) (primarily for yield-bearing wrappers like sUSDe).

### Duration outstanding

Duration outstanding measures total rate sensitivity in Pendle's positions. It's the answer to "if yields move by 1%, how many dollar-years of exposure are affected?"

* Total duration outstanding is [98.9M rate-dollar-years against $546M in OI](https://dune.com/queries/6576943/10388364)

* The weighted average duration is [0.18 years (66 days)](https://dune.com/queries/6576943/10388364), meaning the average dollar on Pendle is exposed to rate moves for roughly two months.

* The [distribution across duration buckets reveals a proportional relationship between capital and risk](https://dune.com/queries/6576901/10388351):

* The majority of capital (70.4%) sits in 30–90 day positions, and those positions carry a roughly proportional share of duration risk (67.2%). This is centered on the March–May 2026 expiry cluster.

* Near-maturity positions (\<30 days) hold 17.3% of OI but contribute only 7.5% of duration risk. The mild inversion appears at the long end: the 12.4% of OI in >90 day positions contributes 25.4% of duration risk.

Pendle functions as a short-to-medium duration venue, not a long-duration funding warehouse. The 66-day weighted average duration, combined with high OI, indicates positioning around specific expiry cycles rather than extended rate commitments.

### OI/Turnover Ratio

Does Pendle's $538M in active OI sit or churn? Dividing each market's outstanding PT by its 30-day PT-notional traded produces a stickiness ratio that can tell us how many months of current turnover it would take to cycle through the entire position.

* The [seven largest markets](https://dune.com/queries/6576969/10388417?sidebar=none) (PT-sUSDe-7MAY2026, PT-reUSD-25JUN2026, PT-srUSDe-2APR2026, PT-sNUSD-5MAR2026, PT-sENA-30APR2026, PT-USDe-7MAY2026, and PT-stcUSD-23JUL2026) collectively hold $529M and all classify as high-stickiness warehousing (ratio >2x).

* PT-sUSDe sits at 107x, meaning its entire 30-day trading volume would need to repeat over a hundred times to equal the outstanding position. PT-USDe shows 60x.

* Even the "lower" ratios in this group – srUSDe at 5.0x, sNUSD at 3.6x – imply positions measured in months of turnover, not days.

* A handful of mid-sized markets (PT-jrUSDe at $15.7M, PT-savUSD at $13.7M, PT-cUSD at $8.1M) show [moderate stickiness with ratios near 1.0–1.6x](https://dune.com/queries/6576969/10388417?sidebar=none), where some active positioning coexists with warehousing.

No market with meaningful OI classifies as an active trading venue. [Roughly 93% of dollar-denominated OI sits in warehousing-behavior markets](https://dune.com/queries/6576969/10388417?sidebar=none). Capital enters, locks a rate, and holds to maturity. The turnover observed is consistent with marginal rebalancing and new entry, not active rate trading or position rotation.

## Implied Rate Curve

The implied rate is the annualized yield embedded in Pendle's Principal Token (PT) prices. When a PT trades at a discount to its underlying SY token, that discount implies a yield to maturity. This curve represents the market-priced cost of future yield across different maturities within Pendle, emerging from the AMM pricing of PTs relative to their underlying assets.

Average implied rate across all active Pendle markets, grouped by asset class shows us:

* [Stablecoin yields trade at 8-20%, while ETH derivatives remain anchored at 3-7%](https://dune.com/queries/6608555/10430811). This percentage point spread persisted throughout 2025. Note that stablecoin PT rates approximate total return, while ETH derivative PT rates compensate only for yield, the holder also carries the underlying's price risk. The gap reflects different risk compositions, not a simple premium.

* ETH derivatives show less volatility than stablecoin yield as a combined asset class.

An important structural note on maturity design: Pendle does not create short-tenor products. Of 182 historical stablecoin markets, 53% were designed with 91–180 day tenors and only 4% with sub-30 day tenors. ETH derivatives skew even longer – no sub-30 day product has ever existed, and 18% of ETH markets carry 365d+ tenors. This means that when short-dated rates appear in the data, they represent aging products approaching expiry, not purpose-built short-term funding instruments. Stablecoin markets are expanding into longer duration, with the 181–365 day bucket showing 16 active versus only 5 expired markets.

### Popular Products by Open Interest

To understand which products drive aggregate rate behavior, we examined implied rates for markets where capital is actually committed.

* Ranking products by current open interest shows the top 10 products by OI are mostly stablecoin-adjacent, no ETH derivative appears. SY-sUSDE leads at $220.6M, followed by SY-reUSD ($85.5M), SY-srUSDe ($81.5M), and SY-sNUSD ($71.3M).

* SY-sENA's ($25.2M OI) average rate of 25.82% with a CV of 34.9% represents a fundamentally different yield profile from core stablecoin funding products.

* Several of the top-10 products (reUSD, jrUSDe, srUSDe, NUSD) only launched mid-2025, meaning their yield statistics cover a shorter observation window than full-year products like sUSDE or USDe.

* High open interest does not imply stable yields. To assess yield predictability, we computed the coefficient of variation for each product, the ratio of rate volatility (standard deviation) to average rate. This normalizes volatility across different yield levels.

* The largest products show wide dispersion in yield stability: SY-sUSDE and SY-USDe exhibit [CV percentages of 43–44.6%](https://dune.com/queries/6609311/10431859), meaning nearly half the average rate level is consumed by volatility.

* By contrast, products like [SY-jrUSDe (CV 12.8%) and SY-NUSD (CV 18%)](https://dune.com/queries/6609311/10431859) offer meaningfully tighter yield predictability.

### Yields: Stablecoin vs. ETH Derivatives

* Within asset class, products move directionally similar. The two asset classes are presented to characterize each rate regime independently. Cross-class rate comparisons do not reflect risk-adjusted relative value.

* In stablecoins:

* Ethena products (sUSDE, USDe) are the only two with full-year coverage, compressing from \~20–23% in January. sUSDE stabilized around 8–10% while USDe drifted to 3–5% by year-end.

* srUSDe, sNUSD, reUSD, stcUSD arrived into a lower-rate environment and traded in the 8–15% range. reUSD stands out as the most volatile of the group, spiking to 20% around July. sNUSD and srUSDe held relatively tighter bands in the 8–13% range.

* stcUSD (Cap) traded the narrowest band of the six until a sharp drop around October, consistent with its low CV of 22.1%.

* ETH-based products cluster around 2–5% with two notable exceptions: SY-tETH spiked to 17% in February and 20% in June 2025. Outside these spikes, ETH products on Pendle offer lower but more predictable fixed yields.

## User Behavior and Capital Concentration on Pendle

This section provides a snapshot of the current state of Pendle, capturing who holds what now and how they behaved up to this point, rather than tracking how these distributions evolved over time.

### Hold-to-Maturity Behaviour

* Across all markets with >1M units of open interest (approximately equivalent to >$1M for stablecoin markets), [85.6% of capital acquired via swaps is held toward maturity](https://dune.com/queries/6617576/10442217). This aligns with the OI/Turnover stickiness ratio: Pendle functions as a funding lock venue where participants acquire PT positions.

* Wallet-level passivity is extreme: [98.9% of buyer wallets never sell](https://dune.com/queries/6617576/10442206) any portion of their position prior to maturity. Early exits are driven by roughly 1% of participants, likely active managers or LPs rebalancing positions.

* Hold rates show no meaningful correlation with market size. [Markets ranging from $3M to $225M OI cluster between 80-100% hold rates, with no systematic decline at larger scale](https://dune.com/queries/6617384/10442139).

* Similarly, time-to-maturity does not materially affect exit behavior. Whether a market has 20 days or 160 days to expiry, hold rates remain clustered between 72-99.6%, with one [outlier market (sYUSD) at 41%](https://dune.com/queries/6617384/10441995).

### Rollover

Rollover analysis examines whether demand for Pendle yield exposure is persistent or episodic. A high rollover rate would indicate wallets systematically re-entering after expiry, demand from participants for the same markets. A low rollover rate suggests one-time tactical positioning.

* Venue-wide swap-based acquisition rollover stands at [7.4%](https://dune.com/queries/6621778/10447159) across $819.3M in expired capital. Only $60.7M (7.4%) that held expired PT positions re-entered the same protocol's next market by expiry. Pendle currently tends to operate primarily as a single-cycle funding lock.

* Variance by market is significant. Rollover rates range from 0.1% (Cap) to 16.4% (Ethena). Ethena's rollover rate accounts for $44.5M in venue-wide rollover capital, while protocols with substantial expired capital bases – Cap at $216.7M, OpenEden at $117.2M – show rollover rates below 1.5%.

* [Only Ethena (16.4%) and Infinifi (13.2%)](https://dune.com/queries/6622157) show rollover behavior consistent with repeat structural use.

The low venue-wide rollover rate has implications for the lending venues that warehouse PT collateral. When PT positions expire without rollover, the associated lending positions – loops, collateral pledges – must also unwind.

### Capital Concentration by Holder Type

Open interest at the wallet level gives us a general idea of who holds Pendle's duration commitments. The distribution indicates whether Pendle serves as infrastructure for retail users or indicates sophisticated use and allocators.

* Pendle is not a direct-to-user venue. Only [20% of total PT OI sits with EOAs interacting with Pendle directly (181M units across 4,079 wallets, excluding Pendle infrastructure)](https://dune.com/queries/6681756).

* The dominant access point is lending protocol integration. Aave, Morpho, Euler, and Silo collectively hold [66.1% of total PT OI (73.8% of external OI) across 76 contracts](https://dune.com/queries/6681756), each aggregating potentially thousands of underlying depositors.

* Aave remains the primary channel: [26 contracts holding 54.7% of total PT OI (552M units)](https://dune.com/queries/6681756). Morpho adds 10.4% (104M units) across just 2 vault contracts. Combined, these two protocols represent 65% of total warehoused capital. Euler (0.8%) and Silo (0.2%) contribute at the margin.

* Multisigs represent 4.2% of OI. This can suggest treasury management or institutional allocations accessing Pendle directly rather than through lending aggregators.

* Wallet counts create an illusion of breadth. The 4079 EOAs sound like broad participation, but they hold only [18% of total units](https://dune.com/queries/6681756). The 76 lending vault contracts holding 66% are the economically significant participants.

* Among direct EOA holders capital concentration remains very high: Gini coefficient of [0.916](https://dune.com/queries/6681766). Pendle attracts concentrated capital both through aggregated lending protocol exposure and among direct participants. The venue does not exhibit broad retail dispersion. Including multisig wallets alongside EOAs produces a near-identical Gini of [0.917](https://dune.com/queries/6681766).

### Holder Composition Across Asset Classes

* Lending protocol integration of Pendle is entirely a stablecoin and "other" asset phenomenon. No lending protocol holds net PT positions in ETH derivatives. [Stablecoin PT is 77.9% Aave, 7.9% Morpho, and only 10.3% EOA](https://dune.com/queries/6623264/10449099). ETH-derivative PT is held entirely by EOA.

* Within lending protocols, asset specialization is pronounced.

* Aave V3 holds 535M units, of which [78.6% is stablecoin and 21.4% "other."](https://dune.com/queries/6623325)

* Morpho holds [61% "other" and 39% stablecoin.](https://dune.com/queries/6623325) The other category includes assets like ENA, CRV, and governance-adjacent tokens and routes disproportionately through Morpho and Euler rather than Aave.

* [Other also carries 3.5% in unclassified contracts](https://dune.com/queries/6623264/10449099), likely specialized vaults or strategy contracts outside of our coverage.

## Yield Tokens: The Other Side of the Split

Every PT minted on Pendle produces a YT as its mechanical counterpart. The split is atomic: 1 SY deposited yields 1 PT and 1 YT and the two cannot be created independently. Total outstanding supply of each is comparable across active markets. But where they end up is entirely different.

* Across 15 active markets with more than 1M units in PT outstanding, YT balances sit almost entirely in individual wallets. [In 12 of 15 markets, more than 93% of YT is held by EOAs.](https://dune.com/queries/6681863/10523619) The three exceptions – sUSDE (76.6%), iUSD (82.7%), and siUSD (53.8%) – show the remainder in non-lending smart contracts that custody YT on behalf of depositors.

* No yield tokens sit in lending protocol contracts across all 15 active markets. By contrast, PT distribution varies dramatically depending on whether the underlying has been accepted as collateral on a lending venue. PTs that have been onboarded [59–99% of PT outstanding sits in lending protocol contracts, with the highest concentration in USDe (99.5%) and srUSDe (95.3%).](https://dune.com/queries/6681863/10523619)

When a participant splits SY to post PT as collateral on Aave or Morpho, the PT moves into a lending contract. The YT stays in the minter's wallet or is sold to another individual on the secondary market.

In principle, buying YT is a directional bet on yield: a participant who believes realized yield will exceed the rate implied by current PT pricing can buy YT and profit from the difference. [YT offers capital-efficient exposure because its price reflects only the yield component, creating leveraged exposure without margin or liquidation risk.](http://docs.pendle.finance/ProtocolMechanics/LiquidityEngines/AMM) We can classify current YT holders by acquisition history: only received YT from the zero address (a mint) versus only from other addresses (secondary market acquisition).

[Stablecoin YT across current Ethereum active markets accounts for approximately 524M units across 2,261 holders:](https://dune.com/queries/6676820)

* 66.1% sits with addresses that only ever received YT through minting. This is consistent with the interpretation that the dominant flow is PT-motivated, where YT remains as a byproduct.

* 18.4% with addresses that both minted and subsequently acquired additional YT through secondary markets. These are addresses that manufactured the split, but also came back to increase yield exposure.

* 15.5% with addresses that never minted at all. This represents genuine yield-long demand from participants who went to Pendle specifically to acquire yield exposure without ever manufacturing the split themselves.

The majority of YT is downstream of PT manufacturing. But a meaningful minority (1/3) reflects independent or reinforced yield-long positioning.

The absence of YT from lending protocol collateral markets reflects structural incompatibility with how lending venues assess collateral. PT's collateral profile converges to par at maturity, allowing lending protocols to set high LTVs. YT decays to zero at maturity and collateral value deteriorates over time regardless of market conditions. In cases where the underlying asset experiences losses, YT absorbs those losses first and can theoretically become negative in value. A lending protocol accepting YT as collateral would require either aggressive LTVs that make borrowing uneconomical or continuous monitoring. And while YT trades through the same AMM pool via flash swaps, the execution path is more complex, involving mint/redeem operations alongside swaps, and liquidation of a decaying asset at a predictable price remains harder than liquidating PT.

## PT Reuse Across Lending Venues

Pendle is part of the stack available to asset managers as a tool to offer higher APY for their vaults and serves users with the ability to acquire more units of an asset per dollar spent. Acquiring Principal Tokens means buying the underlying at a discount to par and locking a fixed rate for a defined period, forgoing the variable yield in exchange for price certainty. What makes this trade worthwhile depends on the underlying.

* For volatile assets, the discount can create a meaningful spread over alternatives. If a PT-stETH's implied yield exceeds the staking rate available, the buyer can capture the difference. This can also amplify if the underlying asset appreciates. A buyer with high conviction that a volatile asset will appreciate by maturity may prefer raw exposure over a predictable income stream, treating the PT as a discounted directional position.

* For stablecoins, the logic differs. The asset will not appreciate, so buying and holding stablecoin PTs delivers a better or worse rate than holding the underlying directly. The discount alone is not large enough to be a compelling strategy on its own. The only way to meaningfully amplify the fixed-rate return is through leverage.

Two observations emerge. First, in our venue analysis we observed ETH derivatives make up a small portion of Pendle's flows. The locked APY available for ETH derivatives does not create a meaningful spread over alternatives such as staking, generating little demand for PT-stETH and other ETH-linked products. Meanwhile, stablecoin rates are higher and capital deployed is far larger, making the fixed-rate locking decision more attractive. Second, because the dominant strategy for extracting value from stablecoins relies on looping, and we know Pendle's open interest is mostly concentrated on stablecoins: large parts of the OI could be reflexive. A portion of the capital warehoused in Pendle may itself have been generated by borrowing against previously warehoused Pendle positions.

## Looping with Pendle

Looping with Pendle works as follows: a participant deposits into Pendle to receive PT, posts that PT as collateral on a lending protocol, borrows stablecoins against it, and re-enters Pendle with the borrowed capital.

Why PTs? As maturity approaches, the discount shrinks toward zero and the collateral appreciates relative to the debt, meaning health factors on the loan improve over time. In stable market conditions, the loan becomes healthier as it ages. PT looping does not make a position liquidation-proof. It reduces liquidation risk compared to looping with volatile collateral like ETH, but the risk remains and arrives from several directions.

* Borrow rate spikes. If the lending protocol's borrow rate rises above the PT's locked-in yield, the loop becomes negative carry. Governance changes to LTV ratios, liquidation thresholds, or delisting of PT collateral markets can also break the loop entirely.

* Depegging of the underlying. A shallow depeg can be offset by the PT's gradual appreciation. However, a rapid depeg can push leveraged positions toward liquidation.

* PT liquidity within Pendle. Liquidity for a specific PT depends on LPs depositing PT and SY into that market's pool. Before maturity, unwinding depends on pool depth. Market stress can cause LPs to withdraw, and new pools with attractive incentives can pull liquidity away from existing markets, draining the exit path that leveraged holders depend on.

* Oracle and infrastructure risk. Oracle malfunction or compromise at any point in the asset stack can force unwinding regardless of position's health.

Participants building leveraged loops through Pendle have strong incentives to stay short-dated: less price sensitivity to yield spikes means less liquidation risk, less time for borrow rates to shift or governance changes to take effect, and faster access to capital for redeployment.

### Estimating Leverage Capacity

The yield routing originates in Pendle's AMM but executes entirely in external lending markets. The scope and parameters of available markets define the strategy's reach. Currently three venues are available on Ethereum: Aave, Morpho, and Euler.

* On Aave, two separate parameters govern leverage: Max LTV and Liquidation Threshold (LT), where Max LTV \< LT \< 1. Users can borrow up to LTV of their collateral value but are not liquidated until LT.

* On Morpho, a single parameter governs both: LLTV (Liquidation Loan-to-Value).

* On Euler, the deployer sets a borrowing LTV and a separate liquidation LTV for each vault-to-vault relationship.

We can estimate leverage capacity using available markets for each venue.

Venue: Aave

Market: [PT-sUSDe Stablecoins eMode](https://vote.onaave.com/proposal/?proposalId=299)

| Parameter | Value | Leverage at Threshold |

| --------------------- | ----- | --------------------- |

| Max LTV | 87.4% | 7.94x |

| Liquidation Threshold | 89.4% | 9.43x |